Professor Satya Narayan Misra in Bhubaneswar, February 8, 2026: In December 2025, Reserve Bank of India (RBI) Governor Sanjay Malhotra mentioned that the Indian economy is in Goldilocks period, there was optimism that the Monetary Policy Committee (MPC) would bring down the repo rate by 25 basis points in their February meeting to give a further fillip to the growth momentum. This was further buttressed by the mega Indo EU trade deal that India concluded and the looming tariff reduction by the USA, our largest trading partner, taking out the dark clouds that shrouded India’s external trade.

Professor Satya Narayan Misra in Bhubaneswar, February 8, 2026: In December 2025, Reserve Bank of India (RBI) Governor Sanjay Malhotra mentioned that the Indian economy is in Goldilocks period, there was optimism that the Monetary Policy Committee (MPC) would bring down the repo rate by 25 basis points in their February meeting to give a further fillip to the growth momentum. This was further buttressed by the mega Indo EU trade deal that India concluded and the looming tariff reduction by the USA, our largest trading partner, taking out the dark clouds that shrouded India’s external trade.

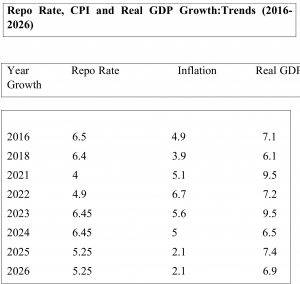

However, the Committee has chosen caution over rate reduction as it is still wary about the likely inflation in the next two quarters of FY 2026-27. All the same, the policy statements show visible confidence that the real GDP during Q1 &Q2 will be 6.9% & 7% respectively, an improvement over their earlier forecast by 20 basis points. This forecast of RBI is also in line with projection made by our Chief Economic Advisor in the Economic Survey that the real growth in the next FY would be in the range of 6.8% – 7.2%. At the same time, the Governor apprehends that the CPI during the next two quarters of FY 2026-27 would be 4% & 4.2% respectively, a near two time jump in CPI witnessed during the FY 2025-26. The inflation prognostication seems to lend credence to a speculation that the RBI has reached the end of repo rate cycle.

MPC after a Decade

One of the transformational policy change in 2016 was constitution of a Monetary Policy Committee to decide the repo rate instead of the one man show of the RBI Governor, assisted by a Technical Advisory Committee. This was a sequel to the Urjit Patel Committee, which recommended constitution of a broad based system, with three outside experts instead of the infernal secrecy that shrouded decision making. The government also chimed in, by making RBI accountable for inflation straying beyond 4+-2%.

In retrospect, the new system is manifestly more democratic and professional as the experts from outside have often differed with the assessment of RBI members. The major factors taken in to account are inflation forecast and RBI as a driver of growth. In the recent past both Prof Jayanth Varma of IIM, and Prof AshimaGoyal reasoned that the RBI Governor’s ostrich like stand in not bringing down the rate with unfounded inflationary expectation stymied India’s growth. Fortunately, after Mr Malhotra has joined in 2025, all the members are in sync and repo rate has been slashed by 125 basic points. It has certainly eased credit flow and abetted growth.

It would be seen from the above, that while the MPC’s decision to increase repo rate to 4.9% in 2022 was justifiably in line with its expectation of high inflation, its intransigence to stick to a very high repo rate for almost 18 months, despite inflation moderating contributed in some measure for growth rate coming down from 9.5% to 6.5% . One can be wise through hindsight. But in all fairness to the two dissenters, RBI Governor possibly did not look at the growth dimension of easy credit on investment sentiment as he should. The present Governor has both been lucky in the matter of food inflation, massive spurt in public investment and benign tax regime.

Inflation Risks

The RBI’s forecast of inflation to be around 4% in the upcoming quarters of FY 2026-27 is predicated on three factors. First, global weather models are flagging the risk of EL Nino conditions developing in 2026. This translates in to uneven monsoon outcomes, with vegetables in particular driving higher headline inflation. Secondly, global commodity dynamics are shifting. Since November, the World Bank’s base metal and minerals index has risen by 15%. Any escalation in geopolitical tensions or supply disruptions could amplify this trend, raising input costs for Indian manufacturers. Thirdly, the forthcoming revision to the CPI series will involve change in sub-indices like food & beverages and housing rent.

The RBI’s forecast of inflation to be around 4% in the upcoming quarters of FY 2026-27 is predicated on three factors. First, global weather models are flagging the risk of EL Nino conditions developing in 2026. This translates in to uneven monsoon outcomes, with vegetables in particular driving higher headline inflation. Secondly, global commodity dynamics are shifting. Since November, the World Bank’s base metal and minerals index has risen by 15%. Any escalation in geopolitical tensions or supply disruptions could amplify this trend, raising input costs for Indian manufacturers. Thirdly, the forthcoming revision to the CPI series will involve change in sub-indices like food & beverages and housing rent.

It is estimated that this could lift measured inflation by around 20 basis points. Against this backdrop, the current pause in reporates well mark the end of rate cut cycle. The RBI has to be complimented for increasing the limit of collateral free loans to MSMEs from the old limit of Rs 10 lakhset in 2010 to 20 lakhs. The RBI has also lifted the ban on banks’ lending to Reits (Real Estate Investment Trumps) .

These initiatives are in sync with the budget announcement of the FM to set up a dedicated SME growth fund of Rs 10000 Cr, and liquidity support through TReDS, which is an RBI regulated platform in India that enables MSMEs to quickly discount invoices from corporate buyers to secure immediate working capital. Access to finance from formal banking sources because of difficulty in providing collaterals has been one of the major handicaps confronting the microenterprises.

Two Wheels of a Chariot

Right from its inception in 1934, the RBI Act swears on its independence from the governmental interference. Osborne Smith, the first RBI governor, resigned on this ground. Dr YV Reddy differed with the then FM Chidambaram on management of FE Reserves and handling of inflation. Dr Raghuram Rajan differed with the government on issues like handling of bad loans and allegedly on demonetisation. However, after resignation of Urjit Patel as RBI Governor in 2018, there is remarkable compatibility between the Mint Street & North Block. This was in evidence when the FM went for a fiscal stimulus. The RBI supported it to its hilt by taking up appropriate follow up measures.

Right from its inception in 1934, the RBI Act swears on its independence from the governmental interference. Osborne Smith, the first RBI governor, resigned on this ground. Dr YV Reddy differed with the then FM Chidambaram on management of FE Reserves and handling of inflation. Dr Raghuram Rajan differed with the government on issues like handling of bad loans and allegedly on demonetisation. However, after resignation of Urjit Patel as RBI Governor in 2018, there is remarkable compatibility between the Mint Street & North Block. This was in evidence when the FM went for a fiscal stimulus. The RBI supported it to its hilt by taking up appropriate follow up measures.

The brief discomfort of the government over the previous RBI governor’s stubbornness in not bringing down repo rate has since dissipated. This has somewhat been helped by India’s benign inflation over the last two years and RBI handing over a massive dividend to the government kitty. It is often said that the fiscal policy and monetary policy should be ideally be two wheels of a nature’s economic chariot to meld the twin objectives of fast growth with moderate inflation. C Rangarajan, the Former RBI Governor used to observe that monetary policy has effective brakes but its potential to accelerate growth is rather weak. In retrospect, this need not necessarily be true.

Leave a Reply

Be the First to Comment!